Municipal bonds have displayed remarkable resilience amid rising interest rates so far, outperforming most yield-related assets. They even weathered the recent government shutdown scare without much ado.

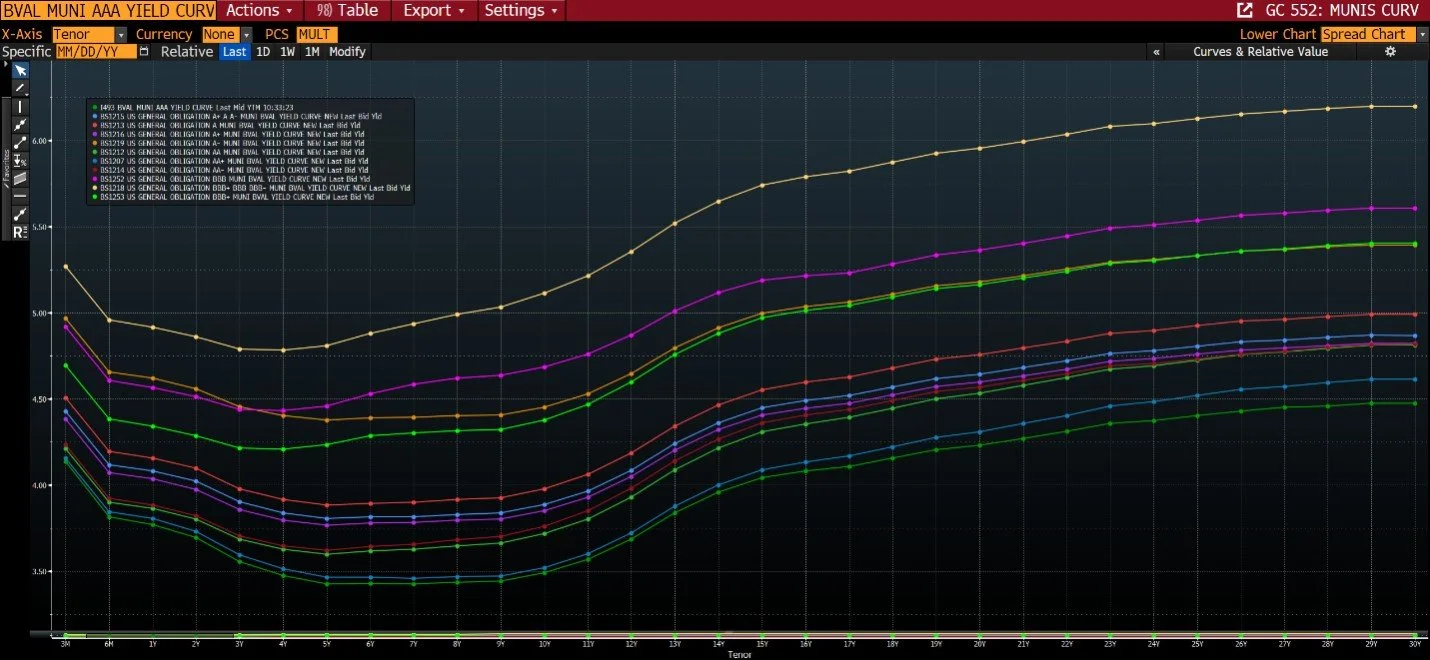

Source: Bloomberg BVAL, AAA Municipal Bond Yield Curve (0 - 40 years), accessed October 3, 2023

Currently, municipal bonds are offering yields at 78% of their Treasury counterparts, which falls within the lower range of historical trends. While it's challenging to pinpoint the exact reason, some may attribute this to a flight to quality. Regardless, considering the broader interest rate context, their stability is noteworthy. For example, the 20–30-year Treasury bonds have declined over 12% year-to-date, including dividends. The MUB ETF has seen a modest decline of -1.8%, including dividends.

Timing plays a significant role in these matters, but presently, we are identifying attractively priced, high-quality municipal bonds. For instance, we've been acquiring municipal bonds with current yields ranging from 3.75% to 4% for short-term maturities and around 5% for mid-term options. Eventually, it will likely become more appealing to explore longer-term bonds. We've been patient in our bond purchases, prioritizing the highest ratings coupled with the best yield offerings. While it may take time, we believe this patience will pay dividends. Tien San Lucas, a Senior Analyst, has done a great job finding and trading these securities.

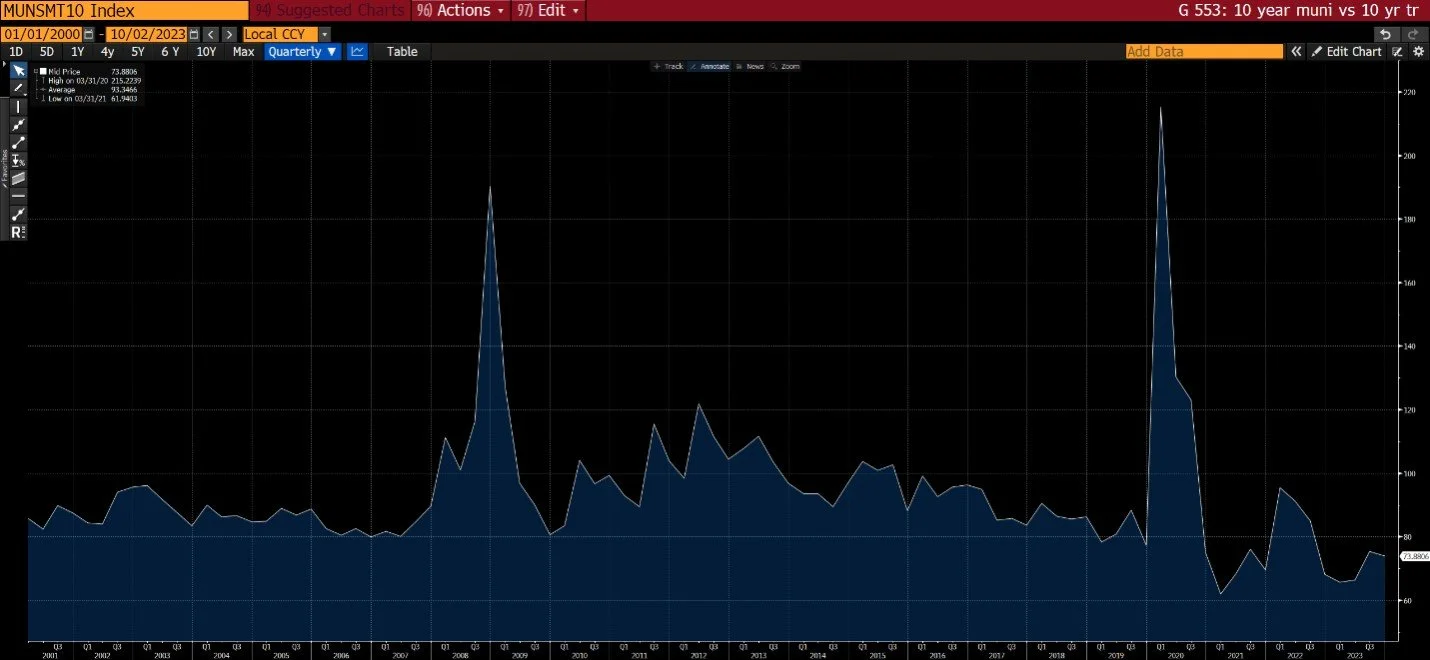

Source: Bloomberg BVAL, 'MUNSMT10 Index from January 1, 2000, to October 2, 2023,' accessed October 3, 2023

The overall yield curve has begun to flatten out over the past two weeks, reflecting the rise in longer-term bond yield, likely due to stronger economic indicators. Moreover, the yield curve has improved from a steep -100bps to a more moderate -22bps.

Additionally, fewer bonds are being called. This is a change from the low-interest-rate environment of previous years, and most liked due to interest rates being at a 17-year high. At this point, we believe that bonds with coupons of 4% or more are more likely to be called, although such instances are rare for older issues.

For clients who have been waiting for an opportunity to invest in high-quality municipal bonds, the current environment presents an auspicious window. Regrettably, those who made purchases 3-5 years ago may find themselves underwater on their principal investments, but we remain committed to exploring avenues to enhance their positions whenever possible.

Please don't hesitate to reach out to our team, if you have any questions or require further clarification.

Gabe Birdsall

This update is being furnished by Brasada Capital Management, LP (“Brasada”) on a confidential basis and is intended solely for the use of the person to whom it is provided. It may not be modified, reproduced or redistributed in whole or in part without the prior written consent of Brasada. This document does not constitute an offer, solicitation or recommendation to sell or an offer to buy any securities, investment products or investment advisory services or to participate in any trading strategy.

The net performance results are stated net of all management fees and expenses and are estimated and unaudited. These returns reflect the reinvestment of any dividends and interest and include returns on any uninvested cash. In addition to management fees, the managed accounts will also bear its share of expenses and fees charged by underlying investments. The fees deducted herein represent the highest fee incurred by any managed account during the relevant period. Past performance is no guarantee of future results. Certain market and economic events having a positive impact on performance may not repeat themselves. The actual performance results experienced by an investor may vary significantly from the results shown or contemplated for a number of reasons, including, without limitation, changes in economic and market conditions.

References to indices or benchmarks are for informational and general comparative purposes only. There are significant differences between such indices and the investment program of the managed accounts. The managed accounts do not necessarily invest in all or any significant portion of the securities, industries or strategies represented by such indices and performance calculation may not be entirely comparable. Indices are unmanaged and have no fees or expenses. An investment cannot be made directly in an index and such index may reinvest dividends and income. References to indices do not suggest that the managed accounts will, or is likely to achieve returns, volatility or other results similar to such indices. Accordingly, comparing results shown to those of an index or

benchmark are subject to inherent limitations and may be of limited use.

Certain information contained herein constitutes forward looking statements and projections that are based on the current beliefs and assumptions of Brasada and on information currently available that Brasada believes to be reasonable. However, such statements necessarily involve risks, uncertainties and assumptions, and prospective investors may not put undue reliance on any of these statements. Due to various risks and uncertainties, actual events or results or the actual performance of any entity or transaction may differ materially from those reflected or contemplated in such forward-looking statements. The information contained herein is believed to be reliable but no representation, warranty or undertaking, expressed or implied, is given to the accuracy or completeness of such information by Brasada.