Brasada Private Accounts

Second Quarter of 2026

“When there is a frenzy of activity in one area of the market there is very often an anti-bubble of discarded companies. In the dot com era these were companies with steady cash flow.”

– Nick Sleep

“Bull markets can obscure mathematical laws, but they cannot repeal them.” – Warren Buffett

Dear Clients and Friends,

We recently announced our newest strategy, Brasada Global Opportunities. Today there are over 5,000 Exchange Traded Funds (ETFs). Some of these ETFs can give us exposure to an international market, theme, or strategy that we can’t really invest in through individual stocks. Global Opportunities is a globally diversified, equity-focused strategy implemented through a portfolio of ETFs. We employ a core-satellite approach here: a foundation of broad-based ETFs providing diversified exposure across U.S. and International equity markets, complemented by satellite positions in ETFs offering targeted thematic, factor, or sector exposures intended to enhance diversification and total return. As the name implies, the Global Opportunities strategy provides broader international exposure than our other strategies, while remaining anchored domestically, with the US as the highest weighting.

Please reach out if you are interested in discussing this new strategy further.

It is not an overstatement to say that the market landscape over the past quarter (and really the past three years) has been one defined by a singular, overwhelming narrative: the rapid evolution, commercialization, and infrastructural buildout of artificial intelligence (AI). Consider that this narrative has been so powerful that, in market terms, it even overshadowed an actual war that broke out between the U.S. and Iran, which as of this writing, will hopefully be winding down during the current 60-day period of negotiations.

That conflict included the closure of the Strait of Hormuz, which historically facilitates the transit of ~20% of the world's seaborne crude oil and liquefied natural gas. The immediate consequences were highly inflationary, with Brent crude oil prices surging toward $120 per barrel and domestic gasoline prices exceeding $4.00 per gallon across the U.S. Simultaneously, the destruction of Qatar's Ras Laffan liquefied natural gas facility knocked ~17% of the nation’s export capacity offline, introducing long-term structural issues to global energy supplies.

These energy constraints acted as a regressive tax on the consumer, crowding out discretionary spending and forcing the Federal Reserve to scale back its projections for interest rate reductions, a hawkish tone which was continued under the new FED Chair, Kevin Warsh. Despite all this geopolitical upheaval, the markets have remained remarkedly resilient, currently hovering around all-time highs.

All Things AI

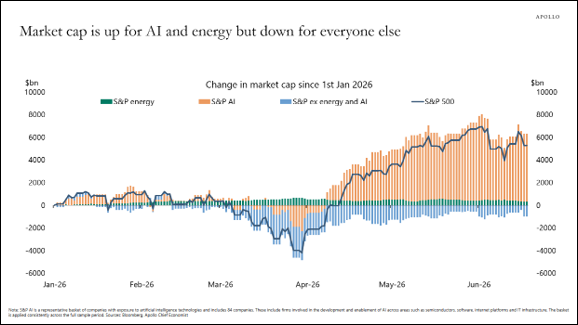

For some context around just how impactful the AI trade has been in supporting the markets this year, consider the following chart from Apollo’s chief economist which shows that if you strip out AI and energy-related stocks, the market would actually be down:

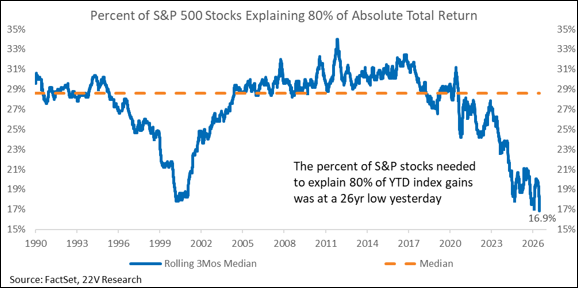

Or consider the following chart from 22V Research showing that the last time so few companies were driving market level returns was just prior to the dot-com bubble popping:

As long-time clients know, markets are cyclical. There are always corners of the market that are temporarily in favor and vice versa. But what we are currently seeing now with this AI-led cycle is something more extreme than what we have seen in the past in that the boom is big enough to move the entire market by itself. This has been amplified by 1) the scale of the demand increase (memory demand has gone up by 400% in a little more than a year due to the AI buildout), 2) the lack of a supply response since it takes years to build more capacity, and 3) the lack of demand destruction that we usually see when prices spike significantly due to subsidization from the leading AI labs and cash flow flush hyperscalers like Amazon, Microsoft, Alphabet, and Meta.

Now, there are numerous reasons to be excited about AI. The broader societal implications of AI should lead to massive productivity gains in our economy, where complex logistical and operational problems are solved through computing, and human capital is freed up for higher-order pursuits. But for investors, while the societal impacts of AI are undeniable, history remains the best guide for how to navigate this environment.

Consider that during the latter half of the nineteenth century, the rapid expansion and construction of the North American railroad network fundamentally altered the economic landscape in a similar fashion, compressing transportation times by orders of magnitude and creating a unified, highly efficient national market. However, the intense capital requirements, fierce competition, and eventual overcapacity that followed resulted in financial ruin for the vast majority of the original investors in those railroads.

Similarly, the advent of the internal combustion engine and the early development of commercial airlines completely revolutionized modern society. Yet again, despite the undeniable, world-altering success of these technologies, almost all the early automobile and airplane manufacturing companies eventually succumbed to brutal price wars and bankruptcy.

More recently, this exact pattern repeated itself with the dot-com bubble, where the overbuilding of telecommunications infrastructure and global fiber-optic networks ended disastrously for investors, even as the resulting physical infrastructure laid the essential foundation for the modern internet.

It has also always been true that early winners aren’t always the long-term winners. In the personal computing era of the 1980s, IBM and later Macintosh were considered the early revolutionaries, but the Windows ecosystem ultimately dominated the market. In the early internet era, Yahoo was the undisputed leader before being completely eclipsed by Google. In the smartphone revolution, Blackberry commanded the lucrative corporate market before the iPhone completely redefined the industry. In social media, MySpace captured the early cultural zeitgeist before Facebook monopolized the sector.

Lastly, it is also important to remember that during every one of these transformative periods, investors seemed to always develop historical amnesia of the periods that came before. When people say “this time is different” are the four most dangerous words in investing, what they really mean is that human nature never changes, and human nature is driven by the greed and fear. In other words, when confronted with highly complex, rapidly evolving technologies that promise to reshape society, market participants frequently abandon traditional valuation metrics in favor of pure, unadulterated price momentum and the speculative hope of winning the lottery on a 1,000% move.

Before we discuss how we are investing in this environment, there is one more topic that we believe is important to understand during this period, the concept of cyclical versus secular.

All Things Cycles

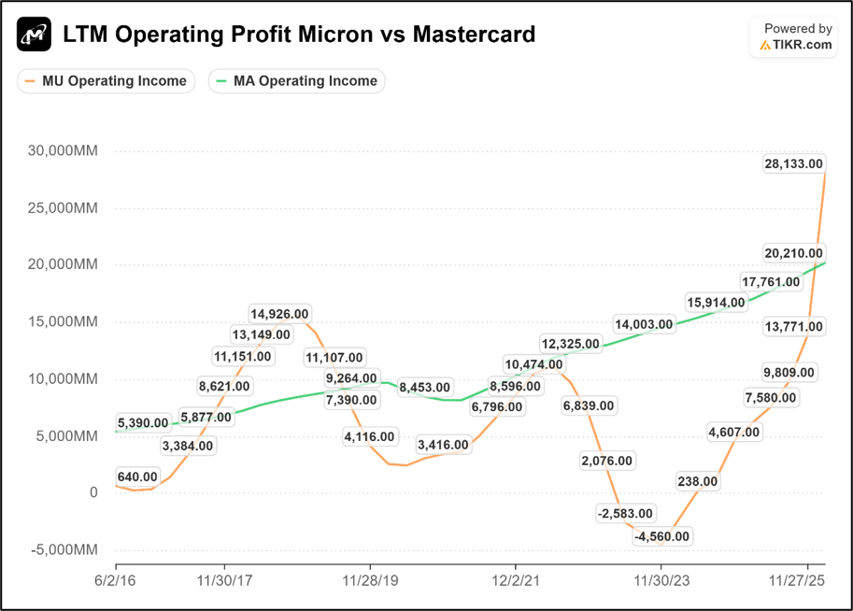

A phrase readers might have heard more often the past year in financial news is something along the lines of: “Memory companies are cyclical” or “The AI revolution will be a secular story for decades to come.” For visual learners, the example below of Micron (a historically cyclical memory business) and Mastercard (a historically secular payments company) may help explain the different concepts here:

Note how Micron’s earnings profile tends to experience ups and downs, good times and bad times, whereas other more secular growers, like Mastercard, tend to have an earnings profile that grows more linearly. Cyclical companies create some issues with how to value them. The most common approach is to take a normalized average of their earnings power through the cycle and then put a multiple on that. Where investors get into trouble is when they start putting a multiple on peak cycle earnings.

In fact, one of the most important questions for investors today is whether the companies supplying the physical infrastructure for the AI boom, specifically certain semiconductor and memory manufacturers that have seen their stock prices 10-fold, have transcended their normal business cycle, thus eliminating the risk of another boom-and-bust cycle in the future.

Once again, history is a good guide here. Consider that in 1970, Intel introduced the first commercial dynamic random-access memory chips (better known as DRAM), but by 1985, Intel was forced to entirely abandon the market that it had invented. What happened was that intense competition within the sector forced manufacturers to surrender any Moore’s Law driven cost savings to their end customers through price deflation.

Effectively, the entire industry was trapped on a cash-incinerating treadmill: manufacturers were required to continuously deploy massive capital expenditures into bleeding-edge fabrication equipment just to maintain parity with competition and falling prices. This seemingly perpetual capital destruction caused an industry-wide wave of bankruptcies and emergency mergers. The number of global memory manufacturers collapsed from more than thirty to an oligopoly consisting of just three players: Micron, SK Hynix, and Samsung Electronics (China’s CXMT is also trying to be a bigger player here).

Despite this consolidation, the industry remained cyclical due to the massive lead times required to construct new fabrication facilities, which make it almost impossible to smoothly match fixed supply with highly volatile end-market demand.

This dynamic can work in the memory companies’ favor when there is a sudden spike in demand, like what we saw with the introduction of artificial intelligence algorithms in late 2022. This created a massive diversion of wafer capacity toward high-bandwidth memory (HBM) production needed for AI, starving the supply chain of conventional DRAM memory, leading to global shortage. Companies like Micron rapidly went from having deep losses in the post-pandemic slump of 2023 to forecasting a staggering $100 billion in free cash flow by 2027.

However, historical precedents, and really the fundamental laws of capitalism, suggest some skepticism about this continuing over the long run. Consider that any industry generating 80%+ gross margins will inevitably attract a competitive response like we saw with the early days of Intel and DRAM. In other words, when a business sector achieves incredibly high profitability, companies naturally respond by pouring more money into expansion. Eventually, this leads to oversupply and ruins the favorable economics that drove stock prices up in the first place.

Because it is impossible to time exactly when this dynamic will play out, these high-flying cyclical businesses do not fit our core strategy, we prefer to have confidence that a sector will remain profitable several years into the future. And as we have talked about before, with more secularly growing businesses, there is usually some kind of competitive moat that prevents competition from entering and driving down profits during the good times. That bucket is where we prefer to search for investments.

How We Are Investing

It is with these historical understandings in mind that we allocate our clients’ capital to this secular AI wave in a more prudent manner. We typically seek to avoid the kind of boom-and-bust cyclical names that might find themselves up very large one year and down very large the next. Instead, we focus on finding the underlying mission-critical infrastructure that must exist regardless of which specific AI future plays out, and which we believe have some kind of competitive moat that will keep competition from driving down profits in the future. Think of the massive data centers, the advanced cooling systems, the baseload energy generation facilities, and the highly specialized networking equipment required to route exponentially growing datasets, which are all inevitable beneficiaries of the recent AI boom.

Furthermore, in environments like this, when investors are throwing money at one in-favor sector, they inevitably ignore other sectors. Today, this means high-quality growth companies, that are unrelated to AI, look cheaper than they have in years. This has allowed us to pair some of our AI “picks and shovels” investments with some great franchises that are currently out of favor, selling at a discount, and where we believe AI will not be a significant risk. The most compelling examples of these types of investments are found in highly mundane industries that have been around for hundreds of years and will likely be around for hundreds more.

Of course, if the AI trade continues to be the only game in town, owning these unrelated to AI businesses will continue to be a drag on relative performance in the short-term. Many investors assume avoiding the highest-flying AI names means missing the AI opportunity. We believe the opposite. Our goal is to own the businesses that will still be earning exceptional returns on capital a decade from now, regardless of which AI models, chips, or software ultimately dominate.

To help you understand these high-quality companies that we are talking about better, below are three short writeups. One on our investment in Amphenol, which we own in our Brasada Equity and Select Equity strategies, which should benefit from the AI buildout. One on Cavco Industries, which we own in our Focused Equity and Select Equity strategies, which is an example of finding value today in more mundane industries. And one on Fastenal, which we own in our Dividend Growth and Equity income strategies, which is somewhere in-between.

Amphenol Corp (APH)

Amphenol is one of the world's largest manufacturers of connectors, sensors, and interconnect systems, essentially producing the nervous system for modern electronics. The company designs solutions that allow power, signal, and data to flow reliably across demanding applications. Rather than selling off-the-shelf commodities, Amphenol acts as a crucial design partner, engineering the vast majority of its 500,000 SKUs as custom or semi-custom solutions tailored to the exact mechanical, thermal, or electrical requirements of its customers.

What makes Amphenol a high-quality business lies in its production of mission-critical components that represent a very small percentage of a customer's total cost of goods. Because the cost of failure is exceptionally high, whether in a commercial aircraft flying at 40,000 feet or a 1,000-volt EV battery, OEMs face significant switching costs and are reluctant to change suppliers once a component is proven reliable. This dynamic is further reinforced by a highly decentralized operating structure where general managers run their business units autonomously, enabling rapid, localized responses to customer needs. Additionally, the company is diversified across eight major end markets, with no single sector accounting for more than 25% of sales, which acts as a powerful shock absorber during cyclical downturns.

Currently, Amphenol is experiencing a supercharged growth cycle driven by the infrastructure buildout in AI. For example, high-speed AI servers designed to train large language models require 50 to 100 times more connector content than traditional enterprise servers to handle enormous power distribution and signal integrity needs. As major hyperscalers like AWS, Azure, and GCP build out their data center clusters, Amphenol provides critical high-speed connectors, fiber assemblies, and backplane systems, effectively acting as the system that allows data to move at hundreds of gigabits per second.

Looking forward, Amphenol's growth runway is also underpinned by the long-term megatrends of electrification and digitization. Whenever an application becomes smarter or more electronic, from factory automation systems and EV powertrains to broadband networks, Amphenol's content per unit naturally increases, creating a persistent flywheel of organic growth. Furthermore, their market remains fragmented and provides a massive ongoing opportunity for Amphenol to execute its proven, countercyclical M&A playbook on top.

Cavco Industries (CVCO)

Cavco is one of the largest producers of manufactured and modular homes, serving as a critical supplier of affordable housing solutions across the U.S. Cavco utilizes 33 manufacturing production lines and distributes its homes through a network of 92 company-owned retail locations as well as independent retailers. To support the entire homebuying lifecycle, Cavco also offers integrated services through its Standard Casualty insurance group and CountryPlace Mortgage finance subsidiary, making it a comprehensive player in the factory-built housing ecosystem.

What makes Cavco a high-quality business is that it operates within a highly consolidated and attractive oligopoly that heavily favors scale and established distribution. The top three manufacturers in this industry, Clayton Homes, Skyline Champion, and Cavco, control more than 86% of total industry production. This concentrated industry structure creates significant barriers to entry for new competitors, allowing the dominant players to maintain rational pricing, and driving outsized returns on capital by leveraging procurement scale and a wide geographic reach. And unlike AI, housing is one of those industries that has been around for centuries and will likely continue to be around for centuries more.

Recent legislative tailwinds, particularly the sweeping bipartisan 21st Century ROAD to Housing Act passed by the Senate in June 2026, are poised to benefit Cavco. Most notably, Section 301 of the Act amends the federal definition of a manufactured home to include housing built with or without a permanent chassis, requiring state certifications to treat them on par with traditional HUD-code homes for financing, sale, installation, and title. Additionally, by establishing HUD as the primary federal authority for safety and construction standards, the bill streamlines the regulatory landscape and expands overall access to manufactured housing. Combined with local zoning changes in certain states that are increasingly permitting manufactured and modular homes in residential areas to combat affordability crises, and Cavco is positioned to expand its addressable market in the coming years.

Looking ahead, Cavco’s long-term growth runway is supported by the structural national housing shortage, which guarantees a sustained need for more affordable housing. This bullish outlook on the multi-year investment cycle of homebuilding was recently validated by Warren Buffett's Berkshire Hathaway, which announced an $8.5 billion acquisition of national homebuilder Taylor Morrison in late May 2026. Berkshire, which already owns the manufactured housing giant Clayton Homes, noted its long-standing commitment to housing and intends to unify its site-built homebuilding operations into a combined platform to capitalize on this strong long-term demand.

Fastenal Company (FAST)

Fastenal distributes a wide array of products including fasteners, tools, safety equipment, and janitorial supplies, but at its core Fastenal is an outsourced procurement and supply chain partner for the industrial sector, helping to seamlessly manage customer inventory. Fastenal embeds itself within its customers’ operations through local branches, automated industrial vending machines, FASTBins equipped with RFID technology, and dedicated Onsite locations where full-time Fastenal employees work directly on the customer’s manufacturing floor. By handling the complexities of sourcing and replenishment, Fastenal ensures parts are always available, allowing clients to focus on their core competencies without the risk of costly production delays caused by a missing screw.

What makes Fastenal a high-quality business is that their customers have come to depend on them for cheap, mission critical parts – any delay or having the wrong type of fastener in inventory can mean millions of dollars in costs for the manufacturers in the form of slowdowns, shutdowns, poor product quality, or recalls. If you’re missing a $0.30 screw on a $10K or $10M machine, you’re just not shipping that machine, and if you have too many of those screws laying around, you’re likely wasting space and money. As such, Fastenal commands premium pricing power, high returns on capital, and reoccurring revenue. On top of that, Fastenal runs a decentralized, highly frugal culture that empowers branch managers to run their operations like entrepreneurs, heavily tying their incentives to localized growth and strict margin discipline.

With roughly 70% of its revenue derived from manufacturing businesses, any acceleration in industrial activity, as we have recently seen with the ISM numbers looking better than they have in years, drives higher consumption of the components that Fastenal supplies. Additionally, the ongoing trend of supply chain reshoring acts as another secular tailwind. As companies bring production back to North America, the construction of new domestic factories and the subsequent increase in localized industrial production expand Fastenal's addressable market. Furthermore, since reshoring often exacerbates domestic labor shortages, manufacturers are increasingly reliant on Fastenal to outsource their supply chain and inventory management functions.

Looking ahead, Fastenal's long-term growth runway remains vast. The company holds just a single digit percent market share in the highly fragmented U.S. fastener market and generates only 17% of its revenue internationally, leaving significant room for geographic and category expansion. Domestically, the company estimates it can expand its footprint of Onsite locations from 2,000 today to 15,000 over time.

Lastly, in addition to traditional manufacturing, Fastenal is benefiting from the AI infrastructure buildout. The construction and maintenance of hyperscale data centers demand an enormous volume of structural components, server racks, cooling systems, power distribution units, and more. Fastenal is a supplier of the more mundane, but critical “nuts and bolts” to many of the companies that manufacture these products as well as physically putting vending machines onsite during data center construction.

As always, we are grateful for your continued trust and partnership, and we are always happy to answer any questions you may have so please feel free to email, call, or come into the office to see us.

Sincerely,

David Shahrestani, CFA

This quarterly update is being furnished by Brasada Capital Management, LP (“Brasada”) on a confidential basis and is intended solely for the use of the person to whom it is provided. It may not be modified, reproduced or redistributed in whole or in part without the prior written consent of Brasada. This document does not constitute an offer, solicitation or recommendation to sell or an offer to buy any securities, investment products or investment advisory services or to participate in any trading strategy.

The net performance results are stated net of all management fees and expenses and are estimated and unaudited. These returns reflect the reinvestment of any dividends and interest and include returns on any uninvested cash. In addition to management fees, the managed accounts will also bear its share of expenses and fees charged by underlying investments. The fees deducted herein represent the highest fee incurred by any managed account during the relevant period. Past performance is no guarantee of future results. Certain market and economic events having a positive impact on performance may not repeat themselves. The actual performance results experienced by an investor may vary significantly from the results shown or contemplated for a number of reasons, including, without limitation, changes in economic and market conditions.

References to indices or benchmarks are for informational and general comparative purposes only. There are significant differences between such indices and the investment program of the managed accounts. The managed accounts do not necessarily invest in all or any significant portion of the securities, industries or strategies represented by such indices and performance calculation may not be entirely comparable. Indices are unmanaged and have no fees or expenses. An investment cannot be made directly in an index and such index may reinvest dividends and income. References to indices do not suggest that the managed accounts will, or is likely to achieve returns, volatility or other results similar to such indices. Accordingly, comparing results shown to those of an index or

benchmark are subject to inherent limitations and may be of limited use.

Certain information contained herein constitutes forward looking statements and projections that are based on the current beliefs and assumptions of Brasada and on information currently available that Brasada believes to be reasonable. However, such statements necessarily involve risks, uncertainties and assumptions, and prospective investors may not put undue reliance on any of these statements. Due to various risks and uncertainties, actual events or results or the actual performance of any entity or transaction may differ materially from those reflected or contemplated in such forward-looking statements. The information contained herein is believed to be reliable but no representation, warranty or undertaking, expressed or implied, is given to the accuracy or completeness of such information by Brasada.