The recent tariff announcements mark one of the most significant changes to American trade policy in decades, and are causing wide reaching impacts. For example, we’ve just witnessed the steepest sell off in the S&P500 since COVID. These new tariffs have caused shock and surprise not just because they are a sharp departure from the free market globalization of the last two decades, but also due to the sheer size of the rates being imposed.

To really understand what’s happening and why, we need to understand what tariffs are, why they’re being introduced, the positives, the negatives and the implications for the economy and for portfolios.

What Are Tariffs?

Tariffs are taxes imposed on imported goods and services, designed to influence trade flows, protect domestic industries, raise government revenue, and advance political aims. As a brief historical background, they were one of the largest contributors to government revenue many years ago, prior to the introduction of income tax in 1913:

How Tariffs Work: A Practical Example

Let’s say a US retailer is importing televisions from South Korea under a 25% tariff:

The retailer purchases TVs at $1,000 each from the South Korean manufacturer

When the shipment arrives at US customs, the importer pays a 25% tariff ($250 per TV)

The total cost rises to $1,250 per TV

The retailer must either:

Absorb the additional cost (reducing profit margins by 25%)

Increase the retail price (potentially reducing sales volume)

Find a domestic or alternative supplier with lower costs

Who Actually Pays Tariffs?

Despite common misconception, it will be the US importer who actually pays the tariff to US Customs—not the foreign manufacturer. However, the economic impact is more complex:

Short-term impact: American businesses importing foreign products or components will see their input costs rise significantly, as they now have to pay customs duties. US consumers will see prices of many popular items rise, as companies try to pass on their higher input costs (this is why tariffs are often referred to as a "stealth sales tax").

Medium-term impact: Foreign manufacturers may lower their prices to remain competitive, absorbing some of the tariff cost. US consumers likely to shift away from purchasing the higher priced foreign goods, or those US goods with high foreign components.

Long-term impact: US importers and manufacturers may try to bring manufacturing and production back to the US, or attempt to source products/components from other countries who have lower tariffs. The intention is that this drives both demand for US goods, as well as US manufacturing.

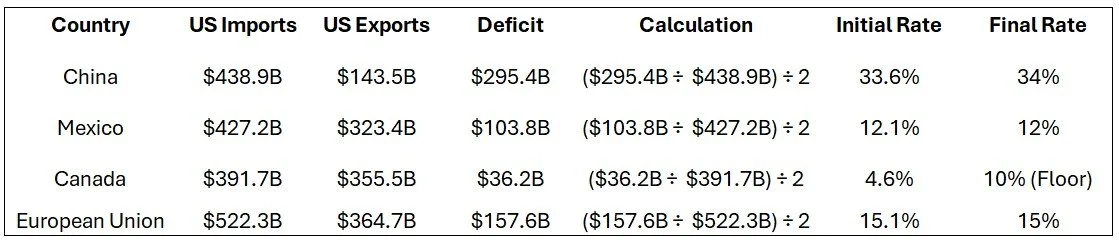

How Tariff Rates Have Been Calculated

The new methodology for calculating tariff rates has attracted a significant amount of criticism and controversy.

The Formula:

Tariff Rate = (U.S. Trade Deficit with Country / Country's Exports to U.S.) ÷ 2

With a 10% minimum floor for any country whose calculation would result in a rate below 10%.

Note: the ‘final rates’ above are in addition to any current tariff in place - for example China already has an existing 20% tariff, so the additional 34% takes the total to 54%.

Technical Criticisms of the Calculation

Elasticity Assumptions:

(Elasticity is a measure of how much the demand of a good changes in response to a change in price. If a small price change leads to a big change in demand, it's considered elastic; if the change is small, it's inelastic. Typically, goods with lots of competition and easy alternatives are elastic- if prices rise you can shop elsewhere, where the more unique items or services are often more inelastic.)

The formula implicitly assumes a price elasticity of imports to tariffs of 0.25, which most studies suggest is closer to 0.945. In real terms, this means it’s likely the calculation is underestimating the impact on demand as a result of tariffs.

Updating this element would cap optimal tariffs at approximately 14% instead of the current rates that reach up to 50%.

The Focus On Trade Deficit Is Fundamentally Flawed

Trade deficits are influenced by many factors, including competitive advantage and global supply chain efficiency. In simple terms: some countries can produce some goods better and more cheaply than others. Punishing efficiency is a net negative for everyone- producers and consumers alike.

As a personal example: you as an individual have a ‘trade deficit’ with your grocery store (you buy more from them than you sell them), but a ‘trade surplus’ with your employer- yet you would not want to impose a tariff on your grocery store, as you do not have the means or ability to grow your own food as efficiently, cheaply, or in such wide variety.

The Case For Tariffs

The current administration's tariff strategy represents a departure from decades of US trade policy that emphasized free trade agreements and lower barriers. Five key rationales have been presented:

Addressing Trade Balances

Objective: Reduce current trade deficits that are viewed as harmful to American manufacturing and employment. The overall US trade deficit has been widening for decades:

Perspective of Supporters: Trade deficits represent "lost jobs" and manufacturing decline in critical sectors.

Perspective of Critics: Trade deficits are natural outcomes of comparative advantage, attempting to reduce them via tariffs will worsen outcomes for all.

2. National Security Considerations

Objective: Maintain domestic production capacity in industries deemed critical for defense.

Implementation: Section 232 tariffs on steel and aluminum aim to ensure domestic supply chains for military equipment and infrastructure.

Example: The US Defense Department requires specialized steel alloys for naval vessels that must be domestically sourced.

3. Intellectual Property Protection

Objective: Combat alleged forced technology transfer and inadequate IP protection.

Implementation: Section 301 tariffs against China specifically target industries where IP concerns are highest.

Context: The US Trade Representative estimates IP theft costs American businesses between $225-600 billion annually.

4. Industrial Policy

Objective: Create space for domestic manufacturing revival, particularly in regions hit by previous import competition. US domestic manufacturing has been declining consistently since the end of WWII:

Target regions: Rust Belt states including Ohio, Pennsylvania, and Michigan.

Economic theory: Temporary protection may allow industries to regain competitiveness through modernization and innovation, but higher prices will be inevitable due to the lower efficiency levels.

5. Negotiating Leverage

Objective: Use tariffs as bargaining tools to secure concessions from trading partners.

Diplomatic approach: ‘Managed trade’ that seeks specific outcomes rather than general free trade principles.

Historical precedent: Similar approaches were used in the 1980s to open Japanese markets to US products.

The Case Against Tariffs

1. Retaliation and Trade Wars

Trading partners have historically responded to US tariffs with counter-measures, and retaliatory tariffs on US goods have already been announced by a number of countries. For example, China have already announced a retaliatory 34% additional levy on US goods.

There is a risk this escalates into prolonged trade conflicts with wide reaching economic effects, which could end up hurting US exports more than any manufacturing benefit.

2. Economic Growth Impact

Financial markets and economic forecast responses have been overwhelmingly negative, there is broad agreement that these tariffs will ultimately prove damaging to the US economy:

Consensus estimates project tariffs will slow US GDP growth by approximately 0.9 percentage points in 2025.

Financial markets are now pricing in expectations for 100 basis points of Federal Reserve interest rate cuts by December 2025, reflecting anticipated economic weakness.

Immediately after ‘Liberation Day’ the S&P500 marked it’s steepest decline since the COVID pandemic as investors and commentators marked down their growth numbers across many industries and companies.

The ICE US Dollar Index (DXY) fell 3% in the 24 hours following the tariff announcement, as investors shifted toward traditional "safe haven" currencies like the Japanese yen and Swiss franc.

3. Inflation Effects

Tariffs are very likely to be highly inflationary and aggressively increase the price of many goods for US consumers. There are 2 main inflationary impacts of tariffs:

A. They function as a tax on imports; increasing the cost of goods. For example, as many component parts of an iPhone are manufactured in China, the cost of production of iPhones will leap under these tariffs, which will ultimately be seen in higher prices for iPhones.

B. Tariffs also drive manufacturing and production to less competitively advantaged and efficient areas, which also increases input costs. For example, forcing more steel production domestically will result in higher steel prices, as US production is not as efficient as some global competitors.

The knock-on impacts of both of these two impacts are hugely complex and may result in the opposite impact than intended. For example:

Automotive: Despite tariffs aiming to protect US auto production, and to reduce imports and purchases of European and Chinese cars, big US manufacturers such as Ford and General Motors are now going to face significantly higher input costs for many components in their cars, which is likely going to raise prices on American-made vehicles alongside their foreign competitors.

Electronics: Approximately 90% of iPhones are manufactured in China, despite Apple’s push to diversify to other areas such as Vietnam and India. However, even those countries are not escaping tariffs, now facing 46% and 26% respectively. Reuters estimates Apple would need to increase iPhone prices by approximately 30% to offset tariffs on Chinese-manufactured components. If Apple were to absorb these costs themselves without passing on to consumers (very unlikely), their ability to continue with leading R&D would be hugely constrained.

Consumer goods: Home appliances, furniture, and clothing prices are projected to rise by 10-20% on average, due to a huge amount of overseas manufacturing, or component parts.

What Can US Companies Do To Protect Themselves?

Businesses are likely to deploy various approaches to manage tariff impacts:

Supply Chain Restructuring

Onshoring / Nearshoring / Friendshoring: Moving production and inputs either to the domestic US, or to countries with lower tariffs. This will increase costs in the short and medium term, as moving and expanding production locally not only brings significant capex requirements, but will also be structurally higher cost due to US wages. Such strategies also take a long time to implement.

Example: Samsung has already begun to shift some TV assembly from South Korea to Mexico and Tennessee.

Product Redesign

Reformulating products to reduce or eliminate tariffed components.

Example: Some furniture manufacturers have reduced the use of Chinese-made metal components.

Price Strategies

Selective price increases on products with inelastic demand.

Absorbing costs on competitive product lines.

Bundle offerings to obscure price increases.

Consumer Adaptation

American consumers will likely adjust purchasing habits:

Increased interest in domestic brands where price differences narrow.

Potential delay of major purchases (automobiles, appliances) given higher costs for both foreign and domestic goods.

Greater price sensitivity and comparison shopping.

Investment and Portfolio Implications

The new tariffs represent a significant shift in the overall cost and competitive landscape for many US and global businesses. Many companies have already seen large share price declines, hundreds of billions of dollars has already been wiped off US stock valuations in aggregate.

In addition, the situation remains extremely fluid, with individual rates (and external retaliations) changing by the day). It’s unlikely that the picture we see today will persist in the medium term. The markets tend to shoot first and ask questions later, as we’ve already seen. We have to closely watch how things progress from here.

The important element is always- what will the long-term impact on underlying free cash flow be. There are many companies who will see extremely limited impact of tariffs, and yet have seen their share prices sell off with the usual approach of emotional blanket selling and passive equity sellers dragging the good down with the bad. In these areas, it’s likely that we’re seeing good long-term buying opportunities.

For some other companies, the impact of these tariffs on the day-to-day operations will fundamentally rewrite their profitability (or now lack of) and create a marked shift in underlying performance. In those areas it’s important that we fully understand what the ‘new world’ for these businesses looks like. There are likely to be some companies whose business model is sadly no longer viable, or at least significantly less lucrative than previously- here huge valuation mark downs are likely to be appropriate.

We also need to be aware of and continually monitor the wider economic impact- the US consumer is likely to bear the immediate brunt of these tariffs and so the knock-on effect on consumer sentiment, savings rates and spending are all key areas to watch closely.

And further still, we need to continually monitor the impact on global trade- negotiations will continue, as will retaliatory tariffs.

On the positive side, there will be some winners, and some US companies and sectors may well see benefits in the medium and longer term.

Without doubt this is a huge shift to both the short and long term of both the US and global economy, and we’re certainly not at the final tariff rates just yet so need to watch closely how things unfold from here.

This post is for information purposes only and should not be construed as an offer or solicitation for the sale or purchase of any securities. Past performance is no guarantee of future performance. The information provided is believed to be from reliable sources, but no liability is accepted for any inaccuracies. Brasada Capital Management, LP is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. If you have any questions, please contact our team.