A Bifurcated Economy In The Age of A.I.

Before commenting on the market, please note that we will be hosting a dinner for our clients and friends at the Briar Club in Houston on Thursday, January 29th. At last year’s event we hosted a luncheon with presentations from each member of the investment team. With both the dinner and the luncheon formats receiving positive feedback, we expect to rotate how we do this each year. Fortunately, our keynote speaker for this year’s dinner will be fan favorite Dan Clifton, the top-ranked Wall Street analyst covering Washington D.C. policy. With so much news coming from our nation’s capital, this will be a good time to hear from him. The invitation and RSVP details may be found here: Client & Friends Dinner Invitation. The event will also be available on livestream.

Now, on to the markets. Coming into 2025, business confidence was surging as inflation moderated, the Federal Reserve adopted a more accommodative stance, and clarity emerged around the election outcome. Capital spending intentions improved and mergers and acquisitions activity began to rebound after a long pause. In short, animal spirits were returning.

That optimism was interrupted by a policy shock. The uncertain and chaotic implementation of the U.S.’s highest tariffs in 93 years resulted in a 19% market correction in just six weeks. This marked the third decline of that magnitude in the last five years. Since World War II, the U.S. stock market has experienced a similar correction only about once every five and a half years on average. In terms of volatility, investors have now endured in half a decade what has historically taken nearly three decades to occur.

What followed was instructive. A full recovery occurred in only seven weeks and well before clarity around tariffs or policy implementation emerged. In 2025 the market once again reminded us of a familiar lesson: stocks tend to bottom when uncertainty peaks, not when it resolves. Periods like this are rarely comfortable, but they are often decisive for long-term results.

On the strength of resilient corporate earnings and enthusiasm for spending in the artificial intelligence (AI) space, U.S. equity markets logged double-digit gains for the third consecutive year. Once again, the seven largest stocks accounted for more than half of the S&P 500’s total return. Historically, it is rare for such a small group of companies to drive most of the index performance in any one year. Never in the post-war period have three consecutive years of double-digit market gains been so narrowly driven by just seven stocks.

Only a decade ago, the top seven stocks represented roughly half the weight they do today, and leadership was far more diversified, spanning six different sectors. Today’s version is dominated by large technology companies, creating a level of concentration risk that we have never seen before.

Since 1950, the U.S. stock market has experienced only five instances of three consecutive double-digit calendar-year gains. In all but one of those cases, the streak ended the following year. The lone exception was the late-1990s technology cycle, which ultimately lasted five years.

A Tale of Two Economies

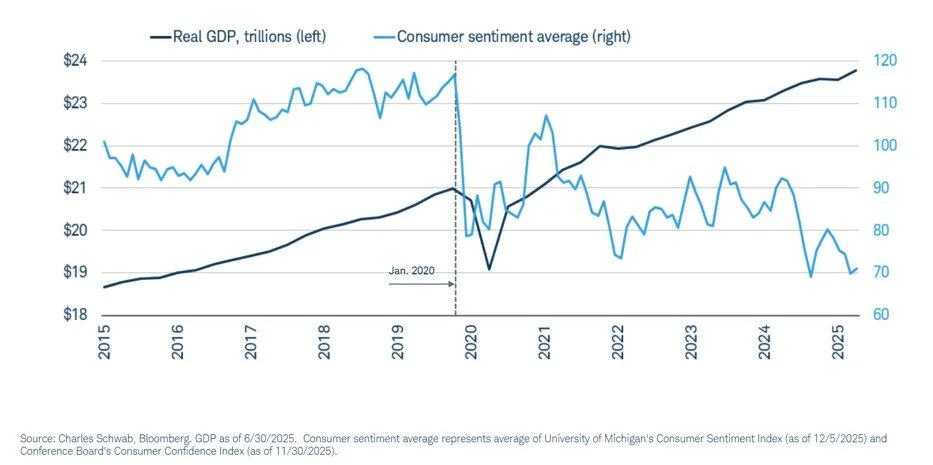

One of the defining features of today’s economic environment is the sharp disconnect between sentiment and reality. Measures of consumer confidence remain near cyclical lows, even as equity markets sit near all-time highs and economic growth is accelerating. Prior to 2020, these measures generally moved together. Since then, they have diverged meaningfully.

This reflects a growing bifurcation in the economy. The cumulative effect of inflation since 2020 has weighed heavily on consumer confidence, particularly among households more exposed to rising everyday costs. By contrast, more affluent households—whose net worth has benefited from gains in financial assets and housing—have been far less affected and continue to spend and invest at elevated levels. As a result, confidence has remained depressed even as consumption and output have held up. The consumer driving a disproportionate share of economic growth is not the same consumer answering the surveys.

This same divide has been evident in the stock market. Much of last year’s performance was driven by a narrow group of companies at the center of artificial intelligence investment. Capital spending on A.I. has been immense, but highly concentrated among firms with the scale and balance sheets required to pursue it. Outside of that group, growth has been more uneven and sensitive to labor constraints, financing costs, and policy uncertainty.

As we look toward 2026, we see more to like than not. The Federal Reserve has begun lowering interest rates with equity markets at or near all-time highs, a combination that has historically been supportive for risk assets. Consumers are also positioned to receive a boost from higher tax refunds and more generous withholding schedules, while corporate investment, particularly in artificial intelligence, remains high. Mergers and acquisitions activity is expected to stay strong, which we view as an important signal of corporate confidence. With inflation continuing to moderate and expectations for earnings growth remaining healthy, the conditions for continued economic expansion look to be in place. More recently the economy has shown signs of acceleration. The last two quarters of GDP growth have been exceptionally strong despite limited job growth, which bodes well for productivity.

On the other side of the ledger, valuations are elevated, the market has already delivered three strong years in a row, and years preceding mid-term elections have often been marked by more muted or volatile returns. These factors do not preclude further gains, but they suggest that progress may be less linear.

Market leadership has been unusually narrow, and it has been a bumpy ride. At the same time, business confidence is improving, capital is being deployed, monetary and fiscal policy are supportive, and corporate earnings remain resilient. While we are never satisfied lagging the market in any given year, we remain confident in the investment process that has served our clients well through decades of market cycles, policy regimes, and economic environments. Periods of extreme concentration have occurred before, and they have not lasted indefinitely. We are not going to concentrate client capital in a single theme, even in an environment where enthusiasm for A.I. remains elevated. When leadership broadens, opportunities tend to expand quickly.

Our equity strategy returns, net of fees, are estimated to be in the mid to high single digits for 2025, except for double digits for Friedberg Focused Equity and Friedberg Equity Income. Our preferred income strategy had its strongest year yet, with double digit returns for 2025, and has a current yield of just over 6%. We are still compiling our composite returns for each strategy and will report on these in more detail in our annual meeting on January 29th.

We appreciate the confidence you have placed in us and wish you the best in 2026.

Sincerely,

Mark McMeans, CFA

This quarterly update is being furnished by Brasada Capital Management, LP (“Brasada”) on a confidential basis and is intended solely for the use of the person to whom it is provided. It may not be modified, reproduced or redistributed in whole or in part without the prior written consent of Brasada. This document does not constitute an offer, solicitation or recommendation to sell or an offer to buy any securities, investment products or investment advisory services or to participate in any trading strategy.

The net performance results are stated net of all management fees and expenses and are estimated and unaudited. These returns reflect the reinvestment of any dividends and interest and include returns on any uninvested cash. In addition to management fees, the managed accounts will also bear its share of expenses and fees charged by underlying investments. The fees deducted herein represent the highest fee incurred by any managed account during the relevant period. Past performance is no guarantee of future results. Certain market and economic events having a positive impact on performance may not repeat themselves. The actual performance results experienced by an investor may vary significantly from the results shown or contemplated for a number of reasons, including, without limitation, changes in economic and market conditions.

References to indices or benchmarks are for informational and general comparative purposes only. There are significant differences between such indices and the investment program of the managed accounts. The managed accounts do not necessarily invest in all or any significant portion of the securities, industries or strategies represented by such indices and performance calculation may not be entirely comparable. Indices are unmanaged and have no fees or expenses. An investment cannot be made directly in an index and such index may reinvest dividends and income. References to indices do not suggest that the managed accounts will, or is likely to achieve returns, volatility or other results similar to such indices. Accordingly, comparing results shown to those of an index or

benchmark are subject to inherent limitations and may be of limited use.

Certain information contained herein constitutes forward looking statements and projections that are based on the current beliefs and assumptions of Brasada and on information currently available that Brasada believes to be reasonable. However, such statements necessarily involve risks, uncertainties and assumptions, and prospective investors may not put undue reliance on any of these statements. Due to various risks and uncertainties, actual events or results or the actual performance of any entity or transaction may differ materially from those reflected or contemplated in such forward-looking statements. The information contained herein is believed to be reliable but no representation, warranty or undertaking, expressed or implied, is given to the accuracy or completeness of such information by Brasada.